Records tumble as nuclear stress spreads beyond France

4 August 2026

Coal demand is hitting seasonal records across Asia even as the European market sends mixed signals. Coal consumption at China's top six power plants surged to 944KT on 3 August — 6% above last year and 12% above the seasonal average — while Vietnamese coal-fired generation jumped 41% year-on-year in June to its highest June level on record. Qinhuangdao domestic prices have edged up to CNY830/t after two weeks of consolidation, and both Russian and Indonesian origins are now competitive for Chinese delivery, with Australian coal back at parity. The fundamental backdrop is strengthening quietly, even as FOB NEWC financial contracts eased $2 on the day to $135.75/t and DES ARA physical ticked up to $122.75/t as the assessment window rolled forward from August to September.

The nuclear stress that has defined this summer in France is now spreading to Central Europe. Hungary has shut down its 2GW Paks nuclear plant for the first time in 44 years after Danube water temperatures approached critical cooling thresholds, removing 40% of the country's domestic generation at a stroke. Romania has declared a state of emergency over its own 1.3GW nuclear plant on the same river, with authorities resorting to detonating rocks in the riverbed to increase water flow. France meanwhile has 7.2GW — over 11% of its entire nuclear fleet — offline due to high water temperatures on the Rhône. The continent's nuclear baseload, designed for a different climate, is proving increasingly ill-adapted to the summers it now faces. Hungary and Romania are likely to turn to coal and gas-fired generation to compensate, adding a new layer of demand to an already tight European market.

The Rhine remains the counterweight: with barges loading at just 30% capacity, ARA coal inventories have built to 3.9mt at HES terminals — 13% above the seasonal average — as coal that would normally flow inland sits at the coast. This is suppressing spot demand at power plants even as clean dark spreads remain strongly positive, with utilities drawing down on-site stockpiles rather than buying fresh spot cargoes. The disconnect between strong generation economics and constrained physical delivery is unlikely to last indefinitely: when Rhine levels normalise, the restocking demand that follows could be sharp.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Markets search for equilibrium as summer volatility persists

31 July 2026

Coal and energy markets are caught in a push-pull dynamic heading into August. DES ARA financial swung $5 higher on Wednesday before giving back $3 the following day, closing at $122.50/t — a pattern of violent intraday moves that reflects ongoing geopolitical uncertainty rather than any clear directional conviction. Spot physical holds at $121/t with the September bid at $119/t, while FOB NEWC is stable around $132/t and the Chinese domestic market has now been unchanged at CNY825/t for two consecutive weeks. Gas and power retain some downside correction potential, with TTF losing 3.2% to €58.60/MWh and German power easing to €137.25/MWh, though EDF's latest nuclear outage figure of 4.9GW — 8% of total French fleet capacity — continues to provide a structural floor. Rhine river levels remain the key physical constraint to watch: German buyers are reportedly delaying spot coal purchases by one to two months, pushing demand into Q4 and supporting the back end of the curve, with Q4 and Cal 27 both firming to $125/t.

The gas-to-coal switching story is broadening geographically. Bangladesh is now a confirmed participant, with coal-fired generation up 27% year-on-year in H1 2026 while gas output fell 8% — a trend driven by persistently high LNG prices and tighter regional supply following the Hormuz disruption. Japan's thermal coal imports rose a solid 34% year-on-year in June, taking H1 imports up 12% to 57.7mt, with Australian and Indonesian supplies both growing strongly. Taiwan's state utility Taipower has issued a fresh short-term tender for 320KT of sub-bituminous coal for October–December delivery, a sign that Asian utilities are actively restocking for the second half. Turkey is also beginning to recover: coal-fired generation rebounded 141% month-on-month in June as hydro seasonally peaks out, and Perret Associates has raised its Q3 coal demand forecast for the country — though on an annual basis output remains 40% below last year's level.

The medium-term picture continues to tighten quietly beneath the near-term noise. EU gas storage is now 10 percentage points below last year's level at the same date. Indonesian exports remain well below 2025 norms. Chinese domestic coal production is constrained by safety inspections following the Shanxi disaster. And with summer not yet over and a fourth European heatwave still working through the system, the conditions for a sustained autumn rally in coal remain firmly in place.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

A second wave — markets test the limits of resilience

23 July 2026

Energy markets are pushing into overbought territory as a second wave of attacks on Iran compounds supply stress that never fully resolved after the first. TTF gas hit €62/MWh — testing the spike seen during the initial US strikes in March — while German power surged 7% to €133/MWh and Brent climbed back above $93/bbl. DES ARA physical reached $123.25/t, though the financial contract showed a potentially significant intraday reversal, surging to $125/t before closing barely changed at $121.75/t — a sign that resistance is being tested and a short-term correction may be approaching. The Rhine remains critically low despite recent rain, with barges running at just one-third capacity; if navigation constraints persist, the coal that utilities need to burn may struggle to reach the plants that need it, even as clean dark spreads make coal-fired generation highly profitable. Separately, a Turkish-flagged coal vessel was struck by a drone in the Black Sea while sailing from the Russian port of Taman, killing one crew member — a reminder that the conflict's reach is extending into supply chains well beyond the Persian Gulf.

China's net steam coal imports rebounded strongly in June, up 29% year-on-year to 30mt, driven by a surge in Indonesian and Australian deliveries. But the H1 total still came in 15mt or 9% below last year, and Russian supplies collapsed 42% year-on-year as sanctions and logistical disruption took hold. The impact is spreading: Indian petcoke production fell in the first five months of the year as crude oil imports via Hormuz were curtailed, and petcoke imports from the Persian Gulf dropped from 7.3mt in H1 2025 to just 4.8mt — tightening the competitive landscape for thermal coal in India's industrial sector. South Korea is confirming a meaningful gas-to-coal switch, with coal-fired generation up 25% year-on-year in the first five months, utilities increasingly substituting high-CV Russian coal for Indonesian grades to maximise efficiency. South African RBCT terminal inventories have surged to a seasonal high of 5.1mt — 42% above the July average — offering one of the few clear sources of additional export supply in an otherwise constrained market.

The week ahead will be shaped by how far the second Persian Gulf escalation develops and whether Rhine levels recover sufficiently to restore normal barge flows. European wind output is forecast to drop well below normal around 24 July before recovering over the weekend, then falling again — a pattern that keeps coal's role in grid balancing firmly intact. With EU gas storage now running 11 percentage points below last year's level and most countries having drawn down reserves during the first wave of disruption, the buffer heading into this second episode is materially thinner. A correction in gas and power is likely at some point, but the medium-term direction for coal remains firmly supported.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Europe's energy rethink deepens as China reopens the arbitrage

21 July 2026

Coal and gas markets in Europe are in overbought territory after a sustained rally, with TTF gas up to €58.45/MWh and German power hitting €125/MWh — a correction is widely expected but has yet to materialise. DES ARA physical is holding just above $119/t, supported by tight availability of qualifying spot material and a Morocco tender awarded $5 above the previous one, signalling that genuine demand is underpinning prices even as the financial curve approaches resistance. The longer-term picture is hardening: the Czech Republic has effectively abandoned its 2033 coal phase-out deadline and is extending its nuclear reactors' operational lives to 2080, joining a growing list of European countries concluding that the energy transition cannot be delivered on the original timetable. State power company CEZ has already raised its 2026 earnings forecast on stronger-than-expected coal generation following gas-to-coal switching triggered by the Hormuz crisis.

In Asia, the most significant development this week is the reopening of the Chinese importing arbitrage. Domestic Qinhuangdao prices have recovered to CNY825/t, bringing Russian and Australian coal back into competitive territory for Chinese delivery — a reversal of the complete arbitrage closure seen last week. The underlying driver is a confirmed decline in Chinese domestic coal production: output across the top four producing regions fell 38mt or 2% year-on-year in H1 2026, with Shanxi hit particularly hard following a mine explosion that killed 82 people and triggered a wave of inspections. India's import trend is also quietly turning — June marked the first year-on-year increase since November 2025, with South African and US grades gradually filling the gap left by declining Indonesian supply, whose share of India's import mix has fallen from 62% in early 2026 to just 51% by May–June.

The structural backdrop continues to tighten in ways that shorter-term price moves do not fully capture. Indonesian export volumes are running well below 2025 levels, domestic PLN allocations are absorbing additional supply through year-end, and Chinese production constraints are proving stickier than expected. Meanwhile the US is on track for a 6% year-on-year decline in coal usage at power plants in July, and EU gas storage remains 10 percentage points below last year's level. The pieces are in place for a more sustained rally once the current overbought conditions in gas and power correct — and coal is likely to follow.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Geopolitics returns, heat bites — DES ARA snaps back

14 July 2026

Energy markets reversed sharply higher this week as hostilities in the Persian Gulf resumed and France's nuclear fleet came under sustained heat stress. DES ARA physical recovered $3.75 to $118.25/t and the financial contract jumped over $5, while TTF gas surged 5.6% and German power hit €117/MWh. The move came after an aggressive and somewhat puzzling $8 sell-off in physical DES ARA late last week — a reminder that summer liquidity can amplify moves in both directions. EDF has now extended outages at three nuclear plants due to Rhône river water temperatures breaching the 30°C regulatory cooling limit, with Golfech, Chooz and Bugey offline until late July at the earliest. A 15% cut in French nuclear output, combined with persistently low Rhine water levels constraining coal barge supply, is shifting the seasonal peak of DES ARA volatility firmly from winter to summer.

In Asia, FOB NEWC is holding support around $129/t while the Chinese domestic market stabilises after weeks of pressure — Qinhuangdao spot is testing CNY805/t and intense typhoon activity is temporarily capping thermal demand while boosting hydro. More strikingly, for the first time this year no international coal origin is now competitive for delivery into China, with even Russian coal flipping to a slight premium over domestic. Chinese power plant coal consumption is running 11% below last year and 4% under seasonal norms, yet stocks remain comfortable — a combination that points to muted domestic output rather than demand collapse. India offers a partial offset: independent coal producers are outperforming strongly at +12% year-on-year in June, even as the two largest state-owned producers continue to miss targets, and the country's sponge iron sector is set to increase its coal-based production share above 80% in 2026 as gas procurement difficulties persist.

Indonesia remains the supply variable that markets cannot ignore. Exports are holding up better than feared at around 1.1mt/day, but the PLN domestic allocation of an additional 4.8mt per month through year-end will progressively reduce the volumes available for export in H2 — and producers who drew down stocks to keep shipments flowing in H1 now have less buffer to work with. The structural misalignment created by the $70/t domestic price cap, unchanged since 2018, is not going away. Whether the government's revised production quotas, expected during July, provide any clarity will be the next key test.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

China softens, Indonesia cracks — the supply story is changing

7 July 2026

The Chinese domestic coal market is weighing on the entire complex this week, with Qinhuangdao spot prices dropping CNY15 to CNY815/t and the importing arbitrage deteriorating sharply — Russian coal now stands as the only origin competitive for Chinese delivery, and even its discount has narrowed to just $3/t, the lowest since the Iran crisis erupted in February. FOB NEWC held flat at $129/t while DES ARA financial sold off aggressively, opening a striking $7 premium of physical over paper for August delivery — a sign that qualifying spot material remains scarce even as sentiment softens. With up to CNY50 of further downside possible in the Chinese domestic market in coming weeks, mid and low CV grades face continued headwinds.

The Indonesia story is proving far less catastrophic than official forecasts suggested, but the cracks are widening. Exports tracked only 3% below last year in May, and Perret Associates now forecasts a full-year decline of 44mt rather than the 190mt collapse the government's 600mt production target implied. The catch: producers appear to have been drawing down stocks to keep exports flowing, leaving less buffer for the second half. The pressure is now acute domestically — over 150 million people in Java alone suffered blackouts in June, and the energy ministry has allocated an additional 4.8mt per month to state utility PLN from August through December. Production quotas are being revised again, and the domestic price cap of $70/t — unchanged since 2018 — remains the root cause of a structural misalignment that no short-term fix will resolve.

In Europe, DES ARA physical is holding firm near $121.50/t even as financial contracts retreat, and the medium-term outlook remains constructive. South African RBCT inventories are rising, up 21% year-on-year, while Turkey continues to confound expectations in the opposite direction — record hydro output has pushed coal-fired generation to its lowest level since 2013, prompting a sharp downward revision to the country's coal import forecast. The divergence between Turkey's hydro windfall and Indonesia's supply crunch is a useful reminder that in commodity markets, the aggregate picture rarely tells the whole story.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Summer heat reshapes the market — a new seasonal dynamic emerges

1 July 2026

Coal markets are finding their footing after weeks of geopolitical-driven volatility. FOB NEWC has confirmed support at $125/t, with spot and prompt paper now trading at parity and the financial curve shifting into a slight contango — a meaningful contrast with DES ARA, which remains in backwardation and is attracting renewed buying interest for August and September delivery. The broader signal is one of stabilisation rather than recovery, though a potentially long and hot European summer is beginning to rewrite the seasonal playbook. Paris is already experiencing localised power cuts as underground cables overheat, and a new heat wave is expected to arrive across Western Europe around 6 July. Falling Rhine water levels are also starting to bite, constraining coal barge supply at precisely the wrong moment.

China's power consumption grew 7% year-on-year in May, with strong momentum across industrial, services and residential sectors — and robust growth is forecast to continue into July. Yet the domestic coal market is softening as precipitation along the Yangtze boosts hydro output, keeping pressure on mid and low CV grades internationally. Russian coal production is rising in response to higher prices, and a partial lift of international sanctions could accelerate that trend further. Meanwhile Australian NSW mine inventories are running 11% below last year's levels, a tightness in supply that is not yet fully reflected in prices but bears watching as the second half of the year approaches.

Turkey stands out as the clear outlier. Record hydro generation — up 58% year-on-year in May — has hammered coal-fired output, which collapsed 67% year-on-year, prompting a sharp downward revision to the country's coal import forecast. It is a reminder that a single weather anomaly can fundamentally reshape a country's import profile within months — and that the medium-term coal demand outlook across emerging markets remains highly sensitive to precipitation patterns as much as to policy.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Peace deal, explosion, election — markets digest a week of contradictions

23 june 2026

Coal markets are in a holding pattern as the dust settles on the US-Iran agreement, with high CV contracts stabilising rather than falling further while the broader energy complex digests a week of conflicting signals. FOB NEWC spot has slipped to $139/t and DES ARA to $116/t, but the pace of decline is slowing. The path back to normal Persian Gulf flows will be anything but straightforward: Monday's severe explosion at the Ras Laffan LNG terminal — killing 13 people and audible 80km away — is a stark reminder that restarting complex infrastructure after a three-month shutdown carries serious risks. More such incidents, whether accidental or otherwise, should be expected in the weeks ahead.

In Asia, the demand picture remains mixed. China's net steam coal imports fell 22% year-on-year in May, tracking well below last year's pace, though a recovery in June is anticipated. Chinese power plant coal consumption is easing off seasonally while inventories remain comfortable. More constructive signals are coming from elsewhere: Malaysia posted an all-time high in thermal coal imports in April, South Korea is showing early signs of gas-to-coal switching, and Indonesia's state power utility PLN is reportedly 20mt short of coal for 2026 — a structural tightness that the low domestic price cap is doing little to resolve. Colombian supply is also back in focus following the narrow election victory of right-wing candidate Abelardo de la Espriella, who has pledged to reverse his predecessor's moratorium on hydrocarbon contracts and lower taxes on the coal sector, though his wafer-thin margin and lack of a party machine make delivery far from certain.

In Europe, French heatwave conditions with temperatures touching 40°C are forcing EDF to cut nuclear output at St Alban, providing a floor for power prices even as gas and coal drift lower. ARA coal inventories are 11% above last year's level but remain 22% below their post-2021 June average — a gap that leaves the market structurally exposed if demand surprises to the upside later in the summer…

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

US-Iran deal in sight — markets reprice sharply

16 june 2026

Energy markets sold off heavily on Monday following the announcement of a US-Iran agreement expected to be signed this Friday, with coal, gas and crude oil all correcting sharply lower. FOB NEWC spot dropped to $149/t while the Q3 financial contract plunged $7 to $138/t, and DES ARA spot shed over $6 to close at $120/t — its lowest level since early April. Brent crude fell 4% to $82.80/bbl, TTF gas dropped nearly 10%, and the spread between June and Q3 paper blew out to $10/t, a sign that markets are repositioning fast. As always, the devil will be in the details: with production sites and export terminals across the region severely damaged, the path back to pre-crisis commodity flows is unlikely to be smooth.

The sell-off masks some important nuances. In South Korea, coal-fired generation was up a robust 36% year-on-year in April with early signs of gas-to-coal switching emerging — a structural shift to watch heading into the cooling season, particularly as nuclear output contracts sharply. Malaysia recorded an all-time high in thermal coal imports in April at 4.9mt, more than double March's figure, with Russian supplies surging. Meanwhile Indonesia's newly formed state export monitor DSI has walked back its more ambitious initial mandate, clarifying it will focus on oversight rather than taking over trading and logistics — a more credible and market-friendly approach than originally feared.

In Europe, the picture is mixed. ARA inventories are 20% above last year's level while Polish stocks are falling sharply year-on-year. The notable exception to today's bearish mood is French power, where EDF issued supply cut warnings at its St Alban nuclear plant due to cooling constraints on the Rhône — a reminder that a heat wave arriving in south-west Europe this week could yet provide a floor for power prices even as gas and coal correct lower.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Markets catch their breath — but geopolitics keeps traders on edge

11 june 2026

Coal markets staged a partial recovery this week after fresh Middle East tensions interrupted the recent downward correction. FOB NEWC spot held around the $150/t mark while financial contracts clawed back some of their recent losses, and DES ARA spot absorbed a sharp $4 single-session drop before the curve stabilised. With Trump reportedly signalling a deal is imminent for the 38th time in as many days, markets are increasingly caught between geopolitical fatigue and the risk of complacency — a combination that rarely ends quietly.

The demand picture is quietly shifting in Asia. Taiwanese thermal coal imports surged 36% month-on-month in May, confirming a trend reversal that Perret Associates had been anticipating, with Australian supplies driving the bulk of the gain as Indonesian volumes continue to fall. India's power plant stockpiles are drawing down steadily — still above the June average but the surplus is narrowing fast. Meanwhile, China's solar sector is confronting a structural overcapacity crisis, with curtailment rates rising and most panel manufacturers now loss-making, a dynamic that reinforces coal's continued role in the country's baseload power mix for years ahead.

In Europe, Germany remains a key market to watch heading into Q3. We forecast coal-fired generation to jump 65% year-on-year as wind output declines and gas picks up ground, while ARA inventories — though rising — remain below their post-2021 seasonal average. Turkey tells a different story, with record hydro output crowding out coal and gas sharply. The divergence across European markets is a reminder that aggregate demand figures rarely capture what is actually happening on the ground.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Coal markets pull back — but the story is far from over

10 june 2026

Coal and energy markets extended their downward correction this week, with the bearish trend that began yesterday showing no immediate sign of reversal. FOB NEWC spot has now broken through the $150/t threshold, while DES ARA shed ground across the curve despite a physical market that remains broadly supportive. The correction appears orderly for now, unfolding in small steps as markets digest the latest signals from Iran and reassess positions built during weeks of almost uninterrupted gains.

Beneath the surface, the fundamentals tell a more nuanced story. China's net steam coal imports continue to track well below last year's pace — down over 14% year-on-year in the first five months of 2026 — while ARA inventories are rising and currently sit 17% below their post-2021 June average. Germany stands out as a key data point to watch: coal-fired generation is forecast to jump 65% year-on-year in Q3 2026 as wind output declines seasonally and gas picks up the slack, a reminder that European demand for thermal coal remains structurally present despite the broader energy transition narrative.

With Brent crude down 3.5% and TTF gas softening, the coming days will hinge on geopolitical developments — particularly over the weekend, when market-moving announcements from the US administration on the Iran situation have a habit of landing while exchanges are closed.

Guillaume Perret

This article is based on our Daily Report, available on subscription.

Contact us to find out more

Coal markets at an inflection point — backwardation signals a new phase

5 june 2026

The FOB NEWC 6000 forward curve has flipped from contango to full backwardation within a week, driven by a $7 surge in spot physical prices and a rush of deal activity that closed the gap with prompt paper. While some consolidation may follow in the near term, the speed of this shift reflects how quickly market sentiment can reprice when fundamentals tighten.

The Iran situation continues to cast a long shadow. A notable side effect is the collapse of Chinese steel exports to the Arabian Gulf, undermining the fragile stabilisation of domestic crude steel output. With Hormuz still effectively blocked, China faces growing economic pressure — pressure that could ultimately draw it into a more active role in resolving the crisis.

In the Atlantic and Med, DES ARA has had a volatile week with daily swings of $3–7, while Colombian supply returning to the market after a Force Majeure is capping some of the recent bullish momentum. In Indonesia, early estimates suggest the new state-owned export control entity DSI may need up to $21bn in working capital — a first real test of government resolve on a project that could reshape global supply flows for years to come.

Guillaume Perret

This news is based on our daily report available on subscription.

Contact us for more information

It’s hot out there….

29 May 2026

Extreme heat across Asia is beginning to reshape energy markets, with early signs of El Niño already driving stronger electricity consumption in countries such as India and Vietnam. Temperatures approaching 40°C, combined with weaker nighttime wind and solar generation, are increasing reliance on coal-fired power despite ongoing supply chain constraints.

At the same time, markets remain trapped between geopolitical uncertainty and tightening fundamentals. Hopes for a potential US-Iran agreement continue to clash with renewed regional attacks, leaving traders focused on the future of the Strait of Hormuz and the direction of global energy flows.

Coal markets are showing mixed short-term signals, with pressure on high-CV grades but a more constructive medium-term outlook emerging. Meanwhile, DES ARA prices appear to be losing momentum as gas and power markets wait for the next geopolitical catalyst…

Our latest reports explore:

• The impact of early El Niño conditions on Asian power demand

• Coal’s growing role in stabilising regional grids

• The evolving US-Iran situation and energy market implications

• Updated FOB NEWC, Richards Bay and DES ARA outlooks

• LNG, TTF gas and European power market analysis.

Guillaume Perret

When geopolitics meets tightening fundamentals, energy markets rarely remain stable for long.

19 May 2026

The global energy complex is entering a phase where uncertainty is no longer temporary noise, but a structural market driver. Across coal, gas and power, resistance levels are being tested while geopolitical tensions continue to cloud visibility.

In Asia, Chinese fundamentals are quietly strengthening. Coal-fired generation remains above expectations while domestic production still struggles to accelerate, creating a market environment that remains unexpectedly firm despite widespread expectations of consolidation. At the same time, arbitrage dynamics between Russian and Indonesian grades are reshaping import strategies across the region.

In Europe and the Atlantic basin, traders are increasingly watching critical technical thresholds in TTF gas, Brent crude and German power markets. Whether these levels hold — or break — may define the next phase of the global energy cycle.

Our latest Daily Report explores the emerging signals behind these movements, including China’s coal consumption trends, tightening ARA inventories, Indonesian pricing developments and freight market direction.

Guillaume Perret

This news is based on our daily report available on subscription.

Contact us for more information

Xi Jinping and Trump meeting this week could be critical

12 May 2026

The closure of the Strait of Hormuz is not only impacting crude oil and oil products (impact on traditional transportation) but also sulphur with a direct impact on EVs. (We will develop this story shortly). Given the importance of EVs in the Chinese economy, this means that China also has a strong incentive to reopen the Strait.

Meanwhile Q1 is already gone for Indonesian exports. April will also be down y-o-y and there are no signs of spot improvement. The country is not reacting that quickly to the recent rally, meaning there could be more upside.

Gas to coal switching: first signs in Bangladesh….

Guillaume Perret

This news is based on our daily report available on subscription.

Contact us for more information

Rally continues

6 May 2026

FOB high CV contracts had a strong start after the long 4-day break (Friday 1st and Monday 4th May off in many countries), broadly following the oil contract. Prices initially surged on reports of further attacks on US military ships and a South Korean oil tanker in the Strait of Hormuz.

But they corrected downward in the afternoon as the US announced that Iran had not broken the cease fire. A more sustainable relief will come from a successful US convoy with a few oil tankers and LNG carriers….

Guillaume Perret

This is an extract of our daily report available on subscription.

Contact us for more information

Good idea

24 April 2026

The recent blockade of the Strait of Hormuz (by Iran and more recently by the US) is giving ideas to other countries.

Some officials in Indonesia are floating the idea that the country is studying the possibility to “monetize” shipping traffic through the Strait of Malacca.

The strait is critical for traffic from the Indian ocean and the Atlantic to South East and North East Asia. Singapore is a major port for refuelling or maintenance, for vessels travelling between the Atlantic and the Pacific.

These are very preliminary announcements as no single country fully controls the Strait of Malacca. The Strait is managed by 4 major countries:

Indonesia which controls the South West part with the island of Sumatra

Malaysia which controls the Northeast part

Singapore which controls the Southern entrance and also the narrowest part of the Strait (only 2.7km, which is less than the Strait of Hormuz).

Thailand is a 4th member of the team of countries managing the Strait of Malacca but with a much lower weight.

Singapore, which wants to defend its pro-business reputation, was prompt to refute the idea.

Guillaume Perret

This is an extract of our daily report available on subscription.

Contact us for more information

It’s a new day in Iran

9 April 2026

Once again it was a last minute change of tactic from the US administration which seems relieved to accept a last minute 10 points proposal from Iran. Meanwhile Israel continues its attacks on Hezbollah in Lebanon and an oil pipeline in Saudi Arabia has been targeted. The volume of LNG passing via Hormuz has doubled from last week but these are probably vessels that have been loaded for a while. The LNG production issue in Qatar is still there and the trend of LNG exports in the coming weeks will be critical.

Guillaume Perret

This is an extract of our daily report available on subscription.

Contact us for more information

Spot NEWC 6000 drops back on Trump’s new gyration

24 March 2026

Energy markets were (again) wrongfooted by Mr Trump's change of tactic. The world was preparing itself for an armageddon with a Monday evening ultimatum for Iran to either free up Hormuz or face the destruction of its power plants. Trump has now prolonged the ultimatum to 5 days citing strong progress in negotiations with Iran, which immediately denied it. Still, most contracts corrected down heavily, happy to catch their breath after 3 weeks of almost uninterrupted gains. Russian coal is now the best Value in Use when delivered to China, India and most countries in Asia. South Korean Gencos are boosting their spot procurement with Russian coal. After a few weeks of stalemate, Chinese domestic prices are picking up to attract more international supplies. Currently only Russian coal is competitive when delivered to China. In a similar scenario to 2022 we expect Chinese imports to drop (moderately) in 2026, but this will be more than offset by a surge in imports from other critical countries. As coal is very much back in favour due to the recent developments, it is time to look again at CCUS as an economically viable technology.

Guillaume Perret

This is an extract of our daily report available on subscription.

Contact us for more information

1991 all over again!

Coal back in its role of secured and affordable energy source during crisis

13 March 2026

The mega announcement by the IEA of the release of 400m barrels from its reserve did not have the expected bearish impact on oil, gas, power and coal. This is a sizable volume but this is equivalent to about 20 days of normal crude oil traffic via Hormuz (20m barrels per day) or 1 month of EU oil consumption. Despite the rhetoric from the US of a potentially “imminent” end of the conflict the situation on the ground is much more complex with regular attacks on the few vessels daring to pass the Strait and that have not been authorised by Iran. Until now the consensus was that Trump would decide when the war is over, proclaiming victory whatever the results might be. But three serious doubts are now emerging.

Firstly, as Anne-Sophie Corbeau pointed out in our Webinar on Tuesday, the issue is not only the Strait of Hormuz, but also the fact that oil and LNG facilities have been partially destroyed in the region (Saudi Arabia, Qatar, Kuwait). Even if Hormuz is fully re-opened tomorrow, it will take weeks if not months to gear up production to normal levels.

Secondly Israel seems to have a much harder line on the conflict and it might want to pursue its effort and inflict more damage even if the US is withdrawing from the conflict.

Lastly and in a worrying scenario, it is not a given that Iran will oblige and free up Hormuz if the US stops their assault. Sensing that the wind is turning, Iran could in fact push its advantage and continue to disrupt global commodity flows, while letting oil cargoes transiting via Hormuz but only for specific destinations such as China.

Our Base Case scenario remains a 4-6 weeks conflict for now, but we would need to see serious bombing of the South West coast of Iran sooner rather than later.

All the above is bullish coal demand and prices. Let’s not forget that the first strong correlation between oil and coal occurred in 1991 during the first Iraq war. At that time many power plants were still running on diesel and the Iraq war accelerated the transition from diesel to coal-fired power plants.

We anticipate some gas to coal switching worldwide in the coming weeks and months. We do not anticipate gas power plants to be converted to coal due to the crisis. But as highlighted in our Webinar, this reinforces our view that many countries will skip the gas transition to some degree.

On another note and let’s not forget this, Indonesia daily exports keep falling, despite the recent announcement from the government of a higher production target at 733mt.

Guillaume Perret

This is an extract of our daily report available on subscription.

Contact us for more information

Gone With The Wind, Wakey-Wakey

4 Feb 2026

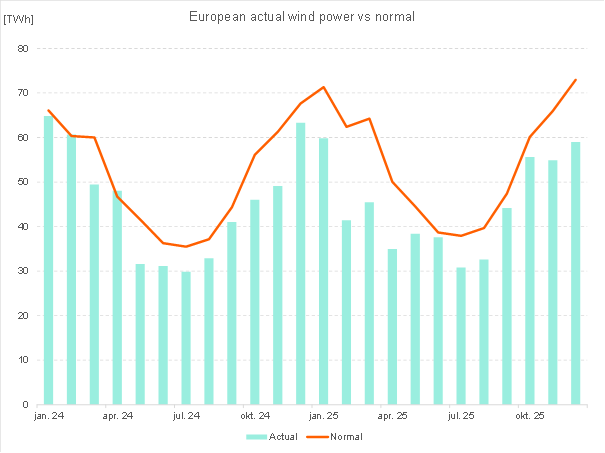

We have been puzzled in our reports by the underperformance of wind generation in recent months, in particular in the EU zone. After a period of strong growth in both capacity (GW) and generation (TWh) during 2010-2022, wind generation in the EU bloc has disconnected with the growth in capacity.

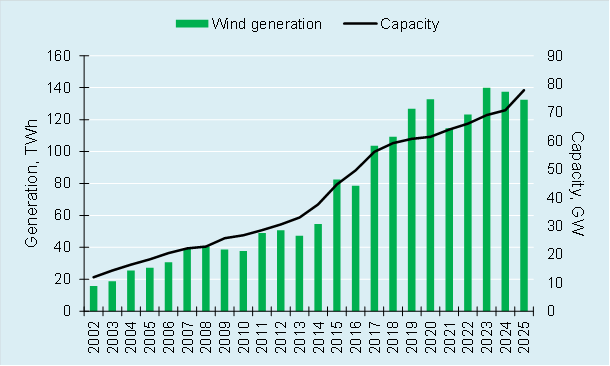

In fact Germany, which is the largest EU country in terms of wind generation, has seen its actual wind generation decrease over the last two years, from its peak of 139.9TWh in 2023 (to 137.5TWh in 2024 and 132.4TWh in 2025). Meanwhile wind capacity increased from 69.1GW in 2023 to 70.8GW in 2024 and we estimate 72-73GW in 2025.

True, the pace of additional capacity has significantly decreased from +3GW to +5GW per annum during 2010-20 and the weather conditions might have changed with lower wind than usual.

But at a EU+ UK level, our colleagues from Volue Data & Forecasts calculate that in 2025, wind generation underperformed by a significant 120TWh vs. what could have been expected based on capacity and normal weather conditions. The under-performance was mainly noticeable during the winter months.

Another reason could be the so-called “wake effect”.

This occurs in wind turbines when some of the energy from the wind is extracted by initial turbines, reducing the energy available to the turbines behind it.

Wind both slows down and becomes more turbulent after it passes through a turbine, which also increases the risk of fatigue damage for downstream turbines.

Research from the University of Colorado has found that the wake effect is stronger offshore. The research predicts that adding more wind turbines in the Atlantic Ocean could reduce the output of existing wind farms by more than 30%.

Most of the reduction comes from wakes formed between turbines within a single farm, but wakes can reach turbines as far as 55km away, so affect other wind farms. The research found that in hot summer periods (when electricity demand is high) wakes last for longer time periods and over longer distances.

There were similar findings in a 2025 study commissioned by the Dutch government, which found overall losses from the wake effect of 21.7%. The Netherlands is aiming to increase installed wind capacity from 5GW now to 70 GW by 2050.

Separate research by Belgian academics found that the effect of adding more wind farms in the North Sea would reduce the annual energy production of 25 out of 69 currently operational wind farms by over 5%, with 13 of them having reductions of more than 10%. The planned Princess Elisabeth zone in Belgian waters is predicted to reduce the output of existing Belgian wind farms by more than 15% in one out of every five 24-hour periods with high production potential.

There are possible workarounds for developers, one of the most obvious being to manage the spacing between turbines. That is obviously easier in the US, for example, than in Europe, due to greater availability of space, but the Trump administration has shown its hostility to wind turbines, often called “wind mills” by Trump.

Co-operation between wind farm operators in neighbouring states will be needed to maximise their efficiency. If such co-operation is lacking, those counting on a rapid acceleration of wind generation capacity are likely to be disappointed.

Wind power also creates its own environmental challenges which will need to be addressed. By 2040, between 10,000 and 20,000 turbine blades will be retired each year in Europe alone. Globally, there will be about 43mt of cumulative blade waste by 2050, and permanent disposal solutions need to be found.

I look forward to meeting you at E World in Essen on 10-11 February on the Volue Data & Forecasts stand (Halle 3).

Guillaume Perret

EU+ UK wind actual generation vs. potential

Source: Volue Data and Forecast

Germany: wind actual generation vs. capacity

Source: Fraunhofer, Perret Associates